Role of NFTs in a Diversified Portfolio

Exploring similarities between traditional art and NFTs

Background

2021 was a breakthrough year for non-fungible tokens (NFTs). NFT became the word of the year. Buyers ranged from your 12 year old neighbour to Fortune 500 CEOs. The success of the overall market induced speculation and we saw numerous copy-paste-projects. However, some collections with loyal communities thrived and became established enough to be sold at traditional auction houses, such as Sotheby’s and Christie’s. While NFTs have many potential use-cases (ticketing, tokenizing real-world assets etc.), the main use case today remains collectibles and digital art (“NFT-art”).

Over the last decade, traditional art has gained the interest of wealth managers as a tool for portfolio diversification. This is mainly due to its low correlation with the rest of the market. Portfolio diversification shows its true strength during times of distress. Given the turbulent markets and weak macro environment we’ve experienced over the past months, it’s a good time to reflect on whether your portfolio is sufficiently diversified.

This piece will explore how NFT-art compares to the traditional art-market, and whether a collection of NFTs could function as portfolio diversification for crypto-native investors.

Why is portfolio diversification important?

Before we get into the weeds, let’s first take a step back and think about why diversification matters.

The golden rule of finance is that return is simply a reward for holding some amount of risk. It is, however, important to understand that there are two types of risks: systematic risks (collapse of the entire market) and idiosyncratic risks (related to individual securities). Market risk is inevitable and hence compensated for. Individual security risk on the other hand can be reduced by diversification. Hence, investors are not compensated for holding it (at least in theory).

For example, if someone is 100% exposed to just one project, their entire portfolio is wiped out if the project fails. This is especially relevant in crypto given that the space is more nascent and there are additional risks, such as smart contract risk or outright fraud. By holding two or more securities which are not perfectly correlated, the volatility of the overall portfolio decreases. The weaker the pairwise correlation, the better.

The same logic applies on a broader scale. If the goal is to maximise risk-adjusted returns, it makes sense not only to add low-correlated assets within the same asset class, but also have exposure to other asset classes.

Overview of the Traditional Art Market

Due to its illiquid nature and fluid definition of what constitutes “art”, it’s hard to get an exact estimate of the value of traditional art markets. However, estimates range between $300-400bn. For argument’s sake, let’s take the midpoint of $350bn as our estimate.

An easier metric to track is annual sales volume. Most art is traded by a few auction houses globally - Sotheby’s, Christie’s and Phillips. In 2021, this number reached $65bn (UBS Art market report 2022), which implies a turnover of less than 20%.

Besides buying a painting merely because it looks good on your living room wall, art has increasingly become a tool for portfolio diversification over the last decade due to its low correlation with the stock market. In addition, financial innovation from companies such as Masterworks has significantly reduced the barriers of entry and democratised the investment process.

With an average annual return of 8.7% over the last 20 years, contemporary art is on par with the performance of gold. In addition, the pairwise correlation between gold and contemporary art is also close to zero, since art isn’t as sensitive to inflation expectations. Therefore, having both as part of a traditional portfolio would be optimal from a diversification perspective.

Overview of NFT market:

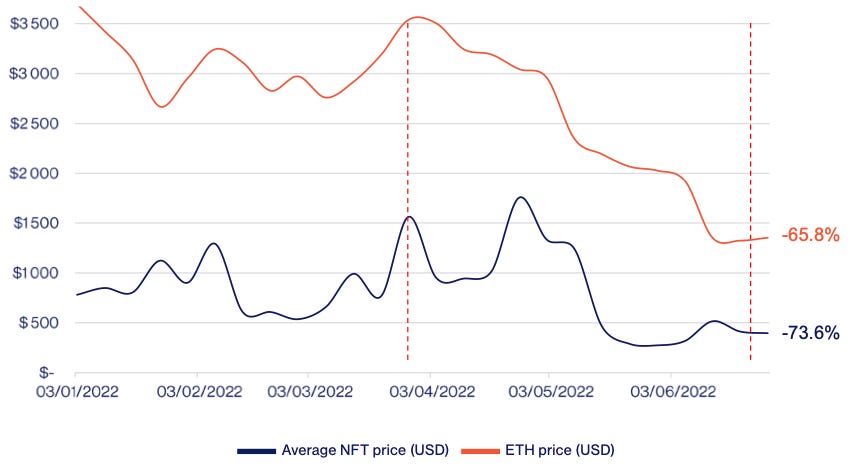

As the adoption of NFTs has grown, so have their valuations. NonFungible estimates the total market value was ~$17bn at the end of 2021. Given the decline in value of ETH, the dollar-value of NFT market is lower today. For a more recent view, we can use data from CoinGecko. Based on 1,213 collections, the current market cap is $7.4bn. There are two caveats: Firstly, Coingecko uses the floor price of each collection to calculate the market cap. Hence, the true value is slightly higher. Secondly, it only includes NFTs on Ethereum. Given this is where most of the value is, it’s not a major issue.

There are three broad observations we can make about the NFT market today:

Value is concentrated in the top collections. 56% of total market cap is within the top 10 collections, and 68% within top 20. This implies that there is a long tail of assets that make up the remaining 32%. The concentration would be even higher, if the data would take into account the value of rare items. While value might become more spread out over time, right now it’s still a “winners take most”-type of market.

Majority of sales volume in dollar terms is still in collectibles and digital art. According to data from NonFungible, there was a total of 10.6m trades with an average price of $1,415 during H1 2022. This implies $15bn worth of NFTs, of which $11.5bn was collectibles and art (~39% of sales volume, ~77% of dollars traded). The numbers are adjusted to only include known and legitimate NFTs, and excludes wash trading and suspicious volume.

Source: NonFungible Gaming stands out with almost half of the trading volume, but only 7% of the value. The average value of gaming NFTs is only $209 - significantly below the total average of $1,415. Sales of gaming NFTs also slowed down significantly during Q2, with an almost 75% drop in volumes compared to Q1.

Source: NonFungible Turnover in 2021 was 5x higher for NFTs than traditional art, even after adjusting for wash trading (105% vs ~20% for traditional art). There are two main reasons:

The NFT market is driven by a speculative frenzy, with flippers seeking a quick profit before moving on to the next collection. This is reflected in the average holding period, which in 2021 was just 48 days, down from 156 days the year before. During Q2 2022, Gaming NFTs (78.8 days) showed the longest holding period, whereas Utilities had the shortest (11.5 days)

Less frictions with buying NFTs compared to traditional art, which induces trade. Rather than having to rely on traditional auction houses, NFTs are more accessible and sold on open platforms (Opensea, Looksrare etc.). In addition, there are no storage or shipping costs involved.

Do NFTs work as portfolio diversification?

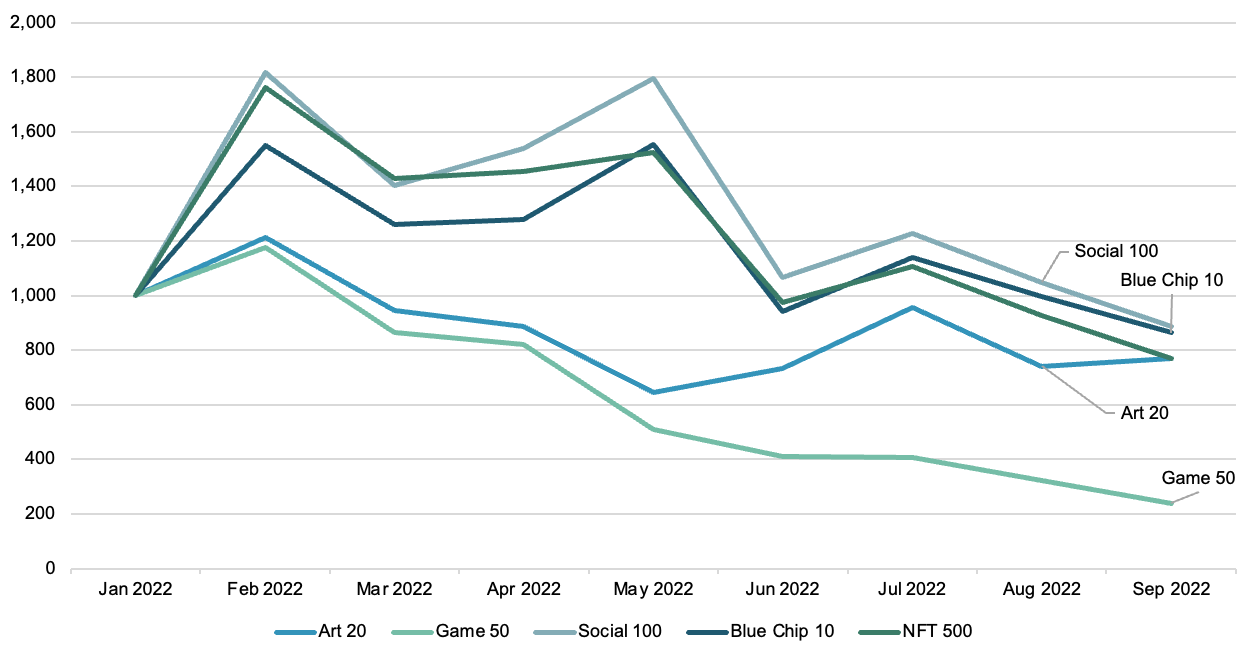

To answer the question on whether NFTs deserve a place in a diversified crypto-portfolio, we can compare their performance to other assets. ETH and BTC represent the wider crypto market, S&P500 the stock market and gold an alternative asset. As a proxy for performance of the NFT market, we use Nansen’s NFT 500, Blue Chip-10 and Art indices. Given the short history of these indices, we are restricted to only YTD performance.

Looking at the table above, it’s pretty clear that exposure to NFTs wouldn’t have saved your portfolio from the downturn. NFTs were resilient during Q1 and outperformed other assets. However, since then they shown high correlation with ETH as crypto started to hit panic mode in early May. Given the significant overlap between holders of crypto and NFTs, it’s expected they move in tandem as traders need liquidity. In addition, general levels of speculation is lower during downturns.

At first look, it seems that the NFT market today is driven by similar forces as the overall crypto market. However, the Art-20 index stands out from the chart below. The crypto crash really got going in the beginning of May, with the fall of Luna, and the rest is history. Since the beginning of May, Art-20 is up 20% relative to ETH, while the rest of the indices are down between 40-50% in ETH terms. This is an encouraging sign, since it is exactly the type of behaviour you would want from an asset used as portfolio diversifier. Stability when all hell breaks loose.

On the one side, this is a very small sample and the outperformance could be fluke luck. On the other hand, it’s not completely unreasonable to believe that the holder base for NFT-art is different to the rest of the NFT market. Someone buying NFTs for the art rather than for speculation sounds naive in today’s world, but maybe there is a hunch of truth in that?

Concluding thoughts

Looking at correlations is not always very informative, especially for young asset classes with small sample sizes. Correlations are inherently backwards-looking and the risk is that dynamics change along with the narrative. A good example is BTC and ETH, which a few years ago displayed almost zero correlation with traditional markets. As the investor base became more “traditional”, BTC and ETH started behaving more in line with other risk assets. Before the crypto-crash, they traded almost 1:1 with tech stocks, making the portfolio diversification argument more difficult to justify. Hence, it’s important to also look at how the narrative evolves over a longer term, rather than just blindly stare at correlations.

Most of the NFT market is still driven by same forces as crypto market. That said, we are seeing some signs that NFT-art is behaving more like traditional art. Artists continue to explore and experiment with new tools at their disposal. Going forward, I expect that the line between what we deem as “traditional art” and NFT-based art will only become blurrier.

Thanks for reading!