Over the last decade, smartphones have grown to become an extension of our arm. Increasingly, they are the primary way we explore the digital world.

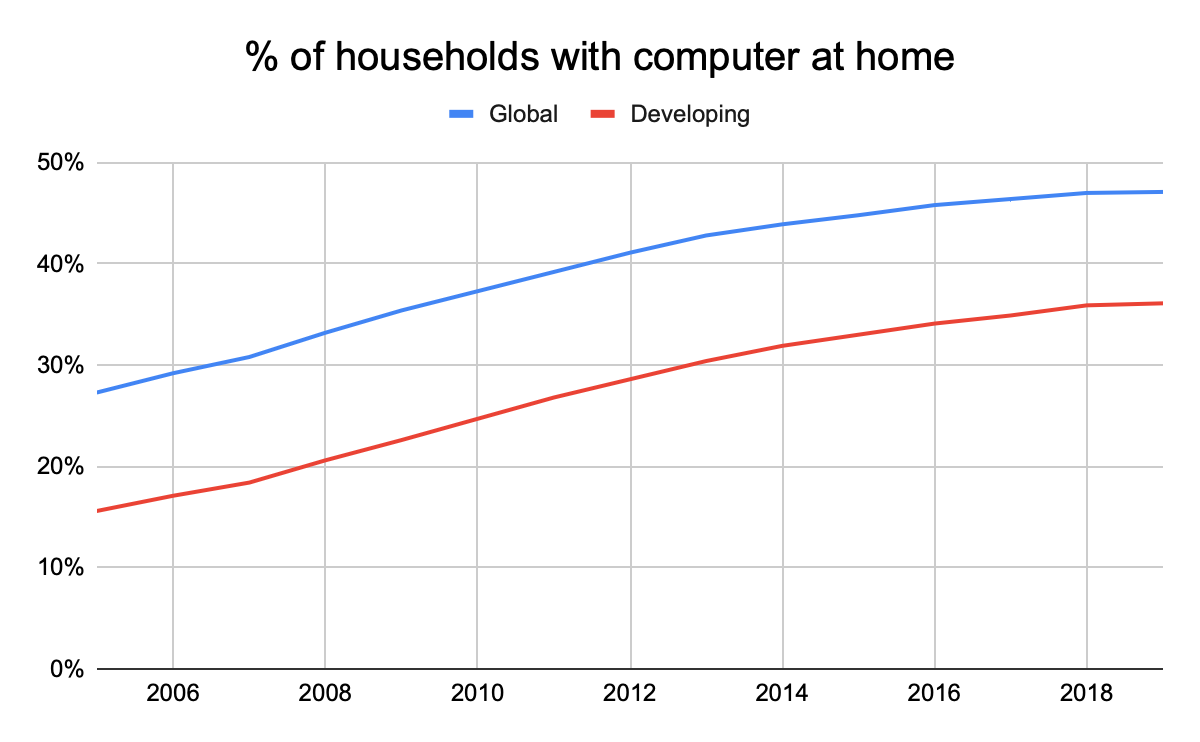

In order for crypto to reach wider adoption, we need mobile. It’s estimated that more than 86% of the population have smartphones. In contrast, less than 50% of households have a computer at home (2019). In developing countries, penetration is even lower. Without mobile, we are leaving a whole segment of users unserved.

Mobile makes interacting with crypto/NFTs and dApps easier, smoother and safer. From a developer’s perspective, it also gives access to mobile-hardware such as GPS and camera, which can be used in the apps. For example, the Move2Earn-apps from last year were already leveraging this (GPS for tracking activity).

But how far have we actually come? And what are the building blocks of the crypto-mobile? Let’s dive in.

Why can’t we use current infrastructure?

Rather than having to build out a mobile infrastructure on crypto-rails, wouldn’t it be easier to use the existing infrastructure? Ideally yes, but unfortunately that doesn’t seem possible.

Mobile-OS is controlled by two centralised players - Apple and Google. They set the rules and decide what’s allowed in their respective app stores. For example, Apple recently raised eyebrows with their plan to extract 30% fees from in-app NFT-sales and restricting the sale of utility-based NFTs. Google’s Play Store has a similar policy (correct me if wrong!).

In this walled garden, it’s very difficult for crypto to reach its full potential. While you can find the most popular crypto apps and wallets in the app stores, their features are highly restricted. For example, apps for NFT-marketplaces OpenSea and Magic Eden only allow users to browse NFTs, not buying or selling. Another example from Coinbase Wallet below:

Today, dApps on mobile devices are second class citizens. Users access them either through in-wallet browsers (Coinbase Wallet, Metamask…) or by using the browser—extension and wallet separately, switching back and forth. Needless to say, the user-experience leaves room for improvement.

In the current environment, it’s hard to see native dApps flourish. They don’t have full control and are subject to the whims of the centralised players. Therefore, we need a new and open infrastructure. So who’s building this?

Mapping out the tech-stack

Below is an attempt to lay out the protocols and projects that are building in the space. Brief description of each one and what their focus is. This is probably an incomplete list, so DM me if you know of anyone else building in the space!

Hardware

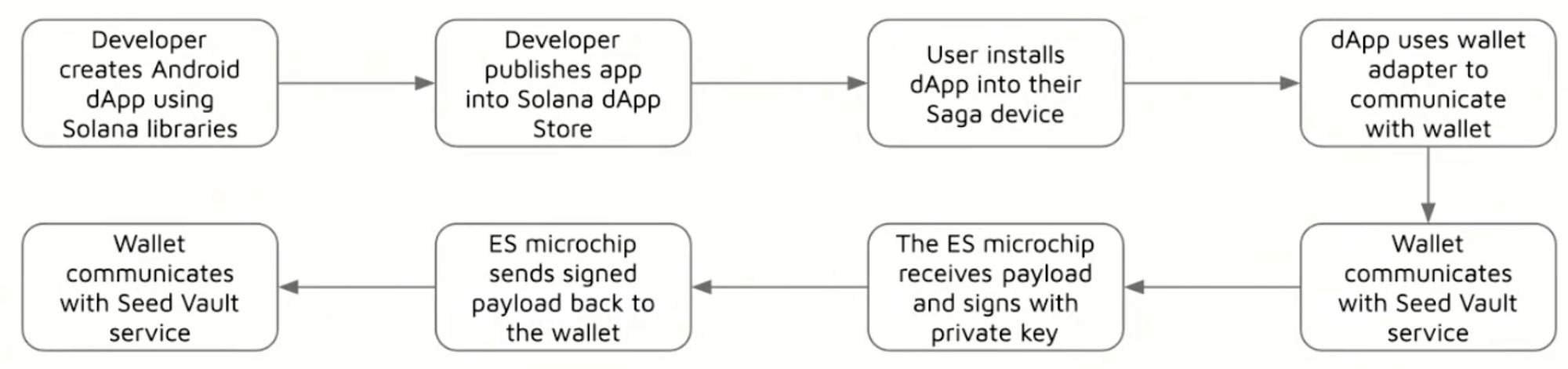

Solana Saga Phone: Saga is a smartphone that’s developed specifically for crypto and web3 (collaboration with Osom). It was revealed in summer 2022 and sells for $1,000. Saga is designed to be your primary device and comes with all the features you would expect from a smartphone. On top of that, it also includes the Solana Mobile Stack (detailed below in more detail) and a key custody mechanism called Seed Vault:

Seed Vault stores your private keys and seeds securely by using the secure element microchip (commonly found in smartphones and used to store cryptographic information such as your fingerprints). With this users get the safety of hardware wallets, while still allowing dApps to easily talk to wallet. All processing and signing happens in the trusted execution environment, which means your keys are never shared with Android or the dApps (more detailed explanation in this interview with Steven Laver, Lead Software Engineer on the project).

Nothing (1): The startup led by Carl Pei (co-founder of Oneplus) is partnering with Polygon to play their part in crypto’s transition to mobile. While the collaboration will start with a simple NFT-drop for early adopters (Black Dot NFT), the ultimate goal is to bring Polygon dApps, games and other crypto-native features to mobile. The ambition sounds similar to Solana’s mobile push, but the path on how to get there is less clear for Nothing and Polygon.

HTC Desire 22 Pro: Branded the “Metaverse-phone”, the Desire 22 Pro is an upgrade from the Binance-branded Exodus 1 (2018). The phone comes preloaded with applications from its metaverse arm Viverse and easy VR-headset pairing, which is where the metaverse name comes from. However, the main feature seems to be the built-in “VIVE” wallet, which can be used to manage your crypto assets and NFTs. The built-in wallet supports Ethereum and Polygon. While it's positive to see one of the traditional manufacturers take a bet on crypto/web3, the Metaverse-phone is otherwise not a particularly impressive smartphone.

Software

Solana Mobile Stack (SMS) is primarily a software kit which gives developers the tools to build native mobile apps, wallets and games on Android. It was released in conjunction with the Saga phone during summer 2022. With SMS, Solana is throwing the ball to developers and asking them to build cool stuff on top of it ($10m funding available!). Main features of SMS include:

SDK and an Android build environment to simplify the developer experience.

Mobile Wallet Adapter that improves the interaction between wallets and dApps, both mobile and web-based. It makes signing transactions on mobile as easy as in a web-browser.

Solana dApp-store is an alternative to the centralised options. An open app-store aimed at Solana mobile apps, without the extractive fees for developers.

Solana Pay is still in development, but the idea is to be able to pay with any token anywhere. Like Google/Apple Pay today.

ethOS: An open-source and community-led project developing a mobile OS for the Ethereum ecosystem. It’s built on top of Lineage OS - the most popular Android fork without the Google-features. While the end goal is to build a full Ethereum phone, developing ethOS is the first step. It’s currently in beta-mode and can be installed on Google Pixel 3, 3XL and 5a. The main features of ethOS are:

Built-in wallet and support for the most popular wallets (Metamask, Rainbow etc). Whether you’re a crypto-novice or seasoned veteran, the goal is to have a crypto-ready experience from the moment you power up the phone. EthOS is taking a similar path to Solana by using the built-in security chip (whenever possible) to encrypt and store private keys.

Running a light-node, meaning your device will verify blocks for itself but doesn’t store all blockchain data. Simplifies the developer experience and means ethOS users don’t need to rely on third party services (like Infura or Alchemy) to interact with the blockchain. In the future it might be possible to move to a full node setup, but this is still one step closer to Vitalik’s endgame - a more decentralised Ethereum.

Decentralised chat (XMTP) that utilises Ethereum and enables messaging to contacts and ENS addresses. Added to the native SMS-messenger app.

Other infrastructure

Helium Mobile: The world’s first crypto-carrier - a 5G mobile network powered by people. It offers a hybrid solution that combines coverage of partner network with the one built by people. Scaling the local network should translate to lower costs for the end-consumer, as Helium becomes less reliant on the partner to provide coverage. Helium recently signed an exclusive 5-year agreement with T-mobile.

The current coverage of the local mobile network is limited with just ~8,000 nodes, but might increase as the network is set to launch in Q1 2023 (waitlist open). For users looking to switch to Helium, the more immediate benefit comes from their data privacy and security. Contrary to incumbents, Helium won’t sell your data and personal information (including location, app usage and browsing history).

L1s that focus on mobile: While the L1-boom has faded, there’s still a lot of them around (and new ones popping up). Some of these are building for mobile, or somehow utilising mobile infrastructure in their protocol design. Two examples of this is Minima and Celo. While they aren’t the biggest protocols by TVL or other measures, we can still learn from their approaches:

Minima is built with decentralisation at its core. The main idea is to allow anyone (including non-technical people) to run a node on their smartphone and help validate the network. So rather than directly focusing on increasing mobile adoption or making it easier for developers, Minima is leveraging mobile infrastructure to power the network. It’s been in development since late 2018 with mainnet launching February 2023. While they pride themselves with a high node-count (+800k in January), traction has been limited with only ~50k downloads for the mobile app (Google Play Store).

Celo is an L1 that’s built from the ground up for mobile. Users onboard using their mobile number and sending a payment is as easy as sending a text. The network maps phone numbers and wallet addresses through a decentralised address-based identity layer. Similar to Minima, mobile participants help secure the network and can earn rewards doing so.

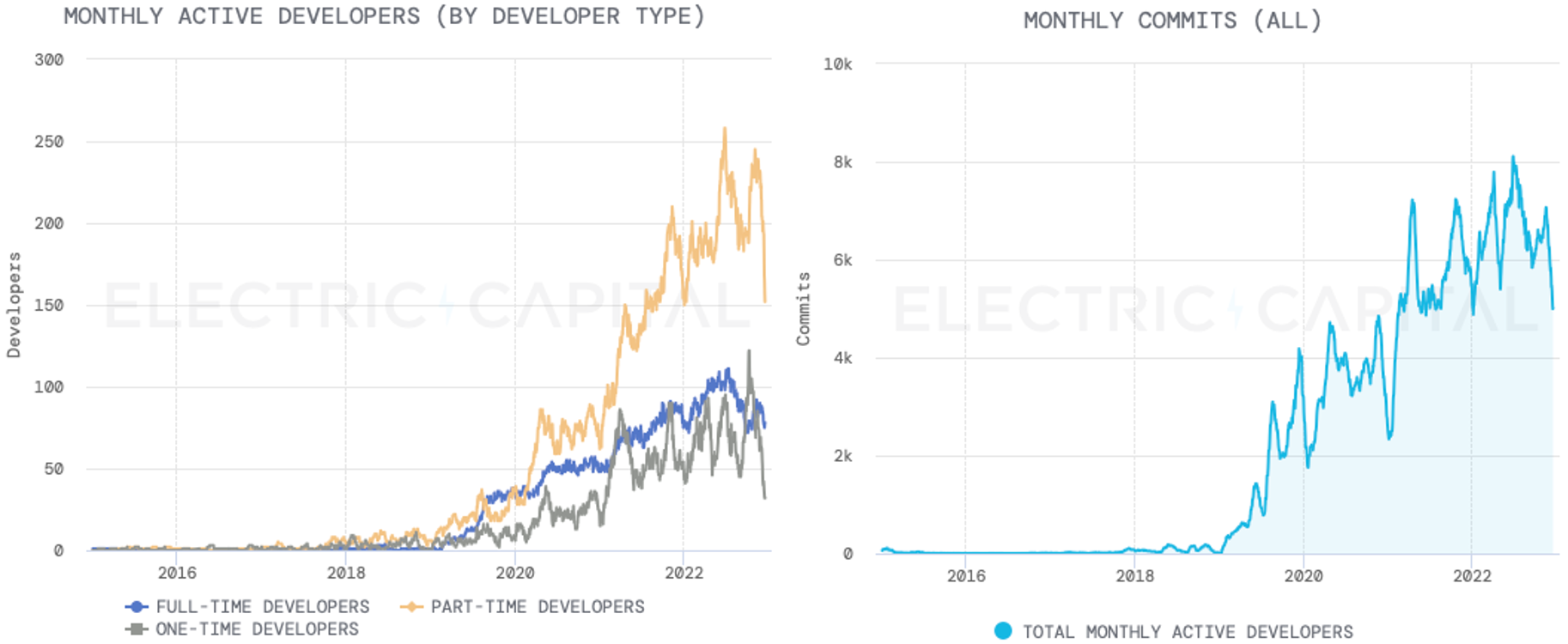

Celo gained traction especially amongst the ReFi-community (Regenerative Finance), but TVL has plummeted since the peak of $1.2bn in November 2021. Despite this, developer activity has remained quite strong with 78 full-time and 262 part-time developers still building on Celo.

Source: Defillama

Criticisms and questions

What if your phone gets stolen? A valid concern and as of now, none of the solutions really talk about social recoverability etc. However, theft and loss of keys are a wider issue for wallets in general, not just mobile. In fact, mobile is improving the security by allowing you to have a hardware wallet in your pocket that’s easy to connect to.

Users don’t want a different device or OS for each chain! It’s true that most efforts today are focused on specific chains. Solana, EthOS and the rest are building for their own ecosystem. The future might see multi-chain or general solutions, but we are still very much in a proof-of-concept stage. In other words, we need to learn to walk before trying to run.

Why now? An important question, given it’s not the first time we’re seeing this. Some of the failed attempts include the Exodus 1 or the KlaytnPhone*. While the more secure mobile-wallet is one argument for it, it’s not enough. For crypto-mobile to succeed, we need a flourishing dApp-ecosystem. Solutions like SMS come with a SDK and other tools, which make it easier for developers to build native dApps. We’ve also seen an influx of developers coming into the space from web2 companies over the last couple years, who should be eager to build. I believe these are the key differences from before.

*Back then it was called BApps (blockchain apps), rather than dApps.

Conclusion

A common thread across projects is increasing security of mobile-wallets and improving user-experience, which are both well-needed!

While it’s unlikely that we’ll see full capitulation from the giants, we are seeing some signs of alignment. In December, it was reported that Apple is considering allowing users to install apps from outside the iOS app-store. However, even if approved it wouldn’t be live until next fall. Crypto moves faster than that.

The fact remains, that we are still very early. What we see today is not the end-goal, but just a first step. But it’s a step in the right direction.