Music NFTs - The new launch platform for small and independent artists?

An overview of the space and key players

Music NFTs is still a niche area within the wider crypto space, but it’s been gaining traction recently. This post will cover:

Overview of the music industry

What are music NFTs?

How can music NFTs add value?

State of the music NFT market

Summary

1. Brief overview of the music industry

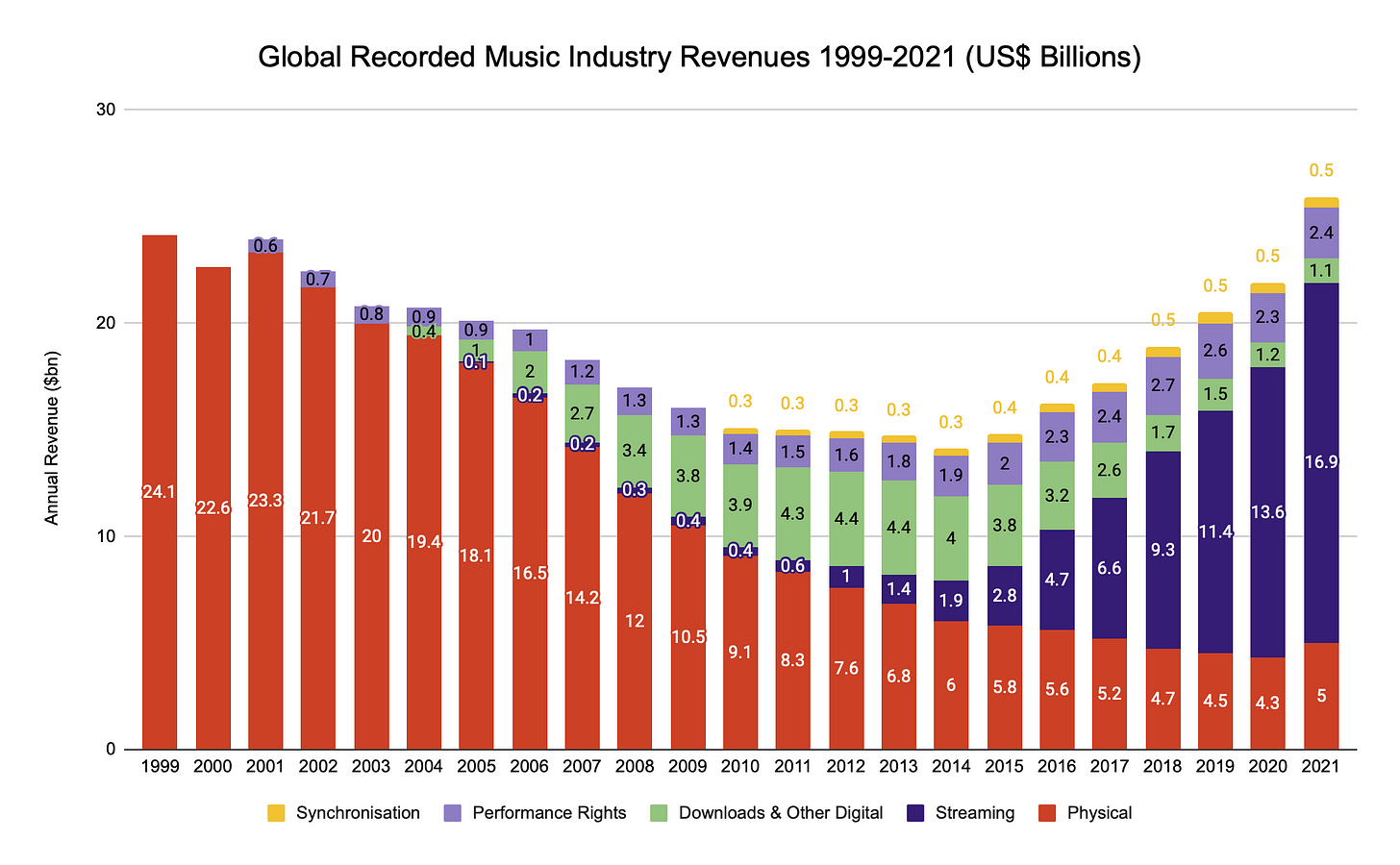

Technology has not only transformed how music is created, but also how it’s being consumed and distributed. Over the past 20 years, we’ve moved away from physical (CDs, Cassettes and Vinyls) to largely digital forms and streaming today.

After years of declining sales, the music industry finally turned a corner in 2015. The growth has continued ever since and revenues in 2021 topped $25.9bn - the highest since 1990 (IFPI).

The primary driver behind this growth is streaming, which today accounts for ~65% of revenues. Spotify is the largest player with ~31% of total paid subscribers and distributed more than $7bn in royalties during 2021 alone.

However, streaming is a double-edged sword. Consumers love it for the convenience and smooth user-experience. For just $9.99/month you get access to pretty much all the songs in the world. For artists however, it’s a slightly different story.

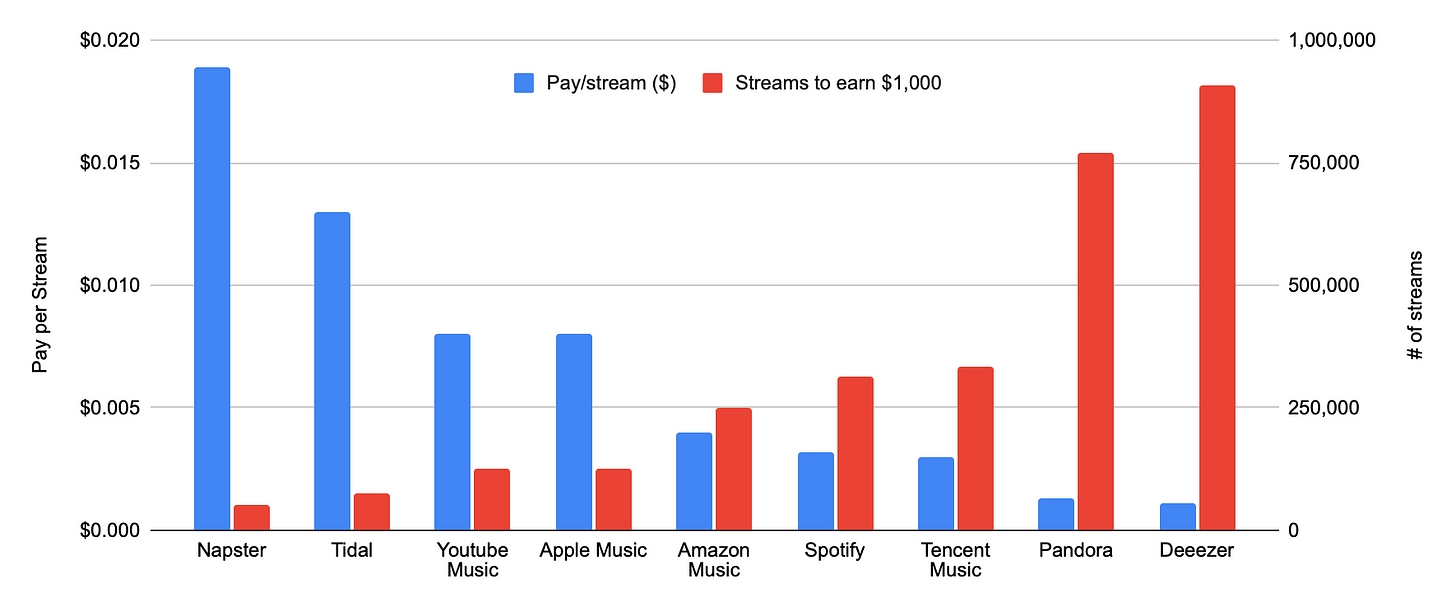

While streaming-royalties work very well for the big names, there is a long tail of artists who barely make anything. In 2021, only 52,000 artists made >$10k off Spotify and 16,500 made >$50k. In context, this is only 0.5% and 0.15% respectively out of the ~11m artists that are listed on Spotify.

While there is some difference in pay/stream between the different platforms, majority of the streams come from Spotify, Apple and Amazon. In addition, the streaming royalty is often further distributed to multiple hands, not just the artist.

For an artist to make any significant money through the streaming-route, they need millions of streams.

Despite its downsides, streaming will continue to exist and grow. But it does beg the question - what other tools are there for artists to monetise and engage with fans? Music NFTs entered the scene as a response to that question.

The aim with music NFTs is to build something complementary that supports artists, not create a decentralised version of Spotify. But before we get too deep into the weeds, let’s first understand what we are talking about here.

2. What are music NFTs?

A music NFT is simply a digital collectible that is linked to music. Broadly speaking, there are two main categories of music NFTs - Art and Utility based. Many music NFTs combine the two in a hybrid model. For example, by buying a song you might also get a share of the royalties or a backstage pass to meet the artist.

The exclusivity of a music NFT is largely dependent on the supply. So far we’ve seen three broad categories on how supply can be determined:

1/1 Edition: Only 1 unique NFT issued. Completely exclusive and similar to a physical art piece. Others can enjoy and listen to it, but only one person can own it. Tends to be sold at a much higher price compared to other editions, due to it’s rarity.

Limited Edition (Limited by supply): A set amount of NFTs issued at a predefined price. Available to mint until supply runs out.

Open Edition (Limited by time): While supply is not pre-specified beforehand, Open ≠ Unlimited. Within the specified time frame, collectors can mint as many NFTs as they want. After that, the supply is set and no new NFTs can be minted.

3. What value do music NFTs bring?

The current benefits of music NFTs centre around monetisation and stronger fan-relationships.

Many independent and emerging artists struggle with the current system. They might have a small and loyal fan-base, but lack the tools to properly monetise it. For larger artists on the other hand, it’s more about identifying the fans with higher willingness-to-pay and focusing on those. The five key benefits are:

An alternative avenue for getting paid:

Music NFTs offer artists another option to monetise their content, in addition to the traditional avenues (touring, record label deals, streaming…). Using data from Sound XYZ, we can see there are a couple artists who made more than $100k last year just from one platform, and several over $50k. For comparison - 1 million streams on Spotify is <$4,000 in royalties.

Emerging artists can also raise money by selling a share of the royalties to an upcoming album. This allows them to access capital without going into debt, similar to a start-up doing a seed-round. The main difference with music NFTs to traditional crowdfunding is that these early supporters share the financial upside with the artist. So it’s a more symbiotic relationship, where everyone can gain from the upside scenario.

Source: SoundXYZ (Sales are denominated in ETH, but translating to dollar terms by using price of $1,500. Artists earn 10% royalty from secondary sales)

All fans are not equal:

Every artist has super fans. These are people who have been there from day 1 and have a higher willingness-to-pay than the average fan. Artists can take advantage of this, and in exchange offer IRL experiences (backstage or access to concerts for life), exclusive merchandise or other personalised experiences.

However, identifying these super fans is not easy. Data from streaming platforms or ticket-sales on individual level is typically not shared with the artists. If they don’t know who these people are, how are they supposed to reach them?

The transparent nature of blockchain enables artists to focus on the super fans. On the other side of a music NFT is a wallet address and a person. The artist can more easily reach out and send additional value through exclusive releases or an invite to a token-gated community with other super fans.

Strengthening the 1,000 true fans-thesis:

The 1,000 true fans-thesis states that creators don’t need millions of followers to make a living. Instead, they can rely on 1,000 fans who are willing to spend $50-100 per year. This would be enough to sustain a decent lifestyle and allow them to continue pursuing their passion.

Similarly, some early web3-artists are proving that they don’t need millions of streams on Spotify. Instead they leverage web3 to make a living off a smaller fanbase. This is particularly valuable for emerging and independent artists, who might otherwise struggle with creating music full-time.

Bankless did a great job of putting things into context with this chart, by visualising earnings from artists on SoundXYZ (in terms of monthly streams) to their actual Spotify streams.

Source: Bankless

Being able to prove you were early:

Many fans attach value to being able to say they were early to an artist. Before music NFTs however, proving you were early to an artists was very difficult. You could create a playlist and maybe receive recognition from friends, but that was about it.

With the help of music NFTs, you can not only prove that you were early and make it part of your identity. Early collectors also share some financial upside with the artist (see point 5)

Making music an investable asset, for everyone:

Over the past decade, music has become an attractive asset class worth billions. Streaming brought more predictability and a longer life to royalty streams, which in turn led to a new-found interest amongst investors. However, so far only institutional investors (mainly private equity firms) and record labels have been able to invest. Not anymore…

Music NFTs are democratising investment in music, similar to how Masterworks has opened up investment in art. Platforms like Royal are allowing fans to buy a share of their favourite artists. While the royalty stream is tokenised, most of the crypto-features are hidden to the back-end, which makes it a smoother experience for the consumer. Since inception a year ago, Royal has already distributed more than $100k in royalties to collectors.

There are non-crypto alternatives for investing in royalties (Songvest, Anote, Royalty Exchange), but these tend to be more restrictive (higher minimum investment criteria and mostly only big artists). In addition, NFT-based solutions makes it easier to bundle royalties with other features, such as the IRL experiences discussed above. This makes it more than just a mere financial investment.

4. State of Music NFT

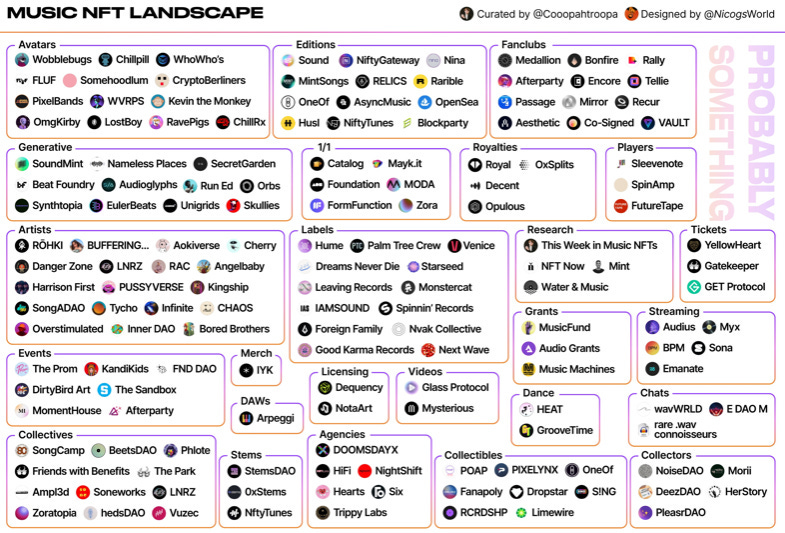

Of course, music NFTs don’t exist in isolation. There is a whole ecosystem around them, including everything from marketplaces and launch-platforms to record labels, fan-clubs and ticketing. I’ve previously written about NFT ticketing, GET Protocol and web3 identities, which all feed into this as well.

The picture below is not an exhaustive list, but gives a good overview of various stakeholders:

Despite challenging market conditions, music NFTs have faired well and shown decent traction recently. This is visible when you take a closer look at the numbers:

The two large marketplaces for emerging artists are Catalog and Sound:

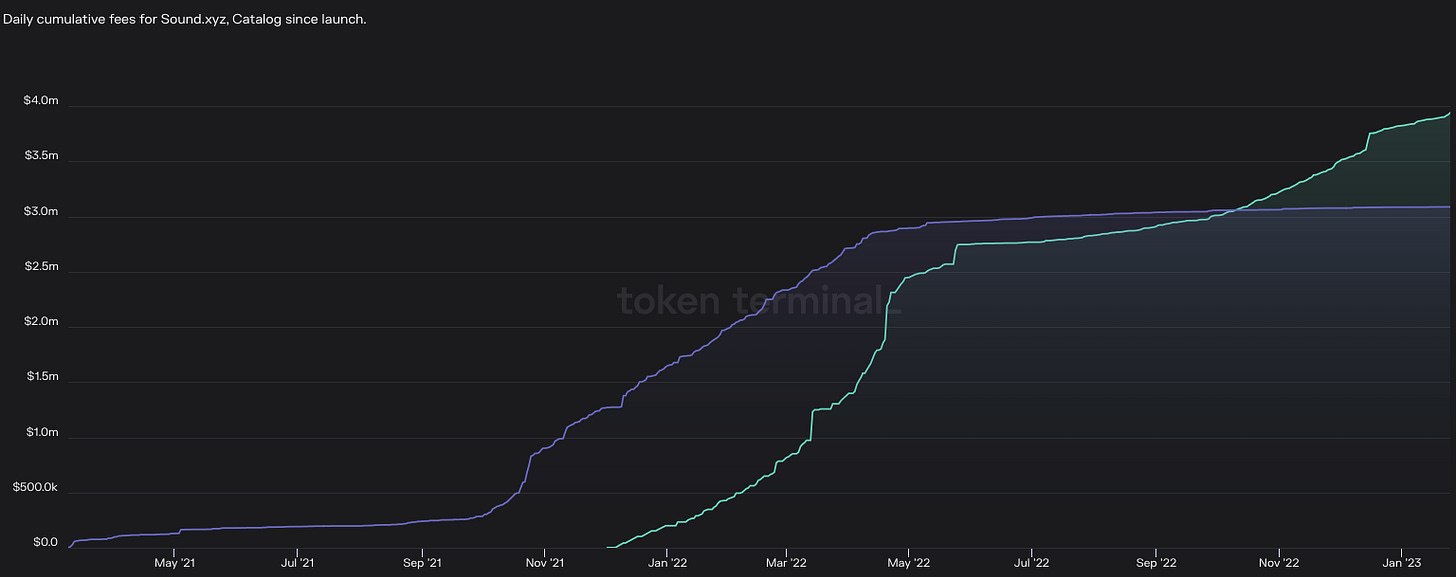

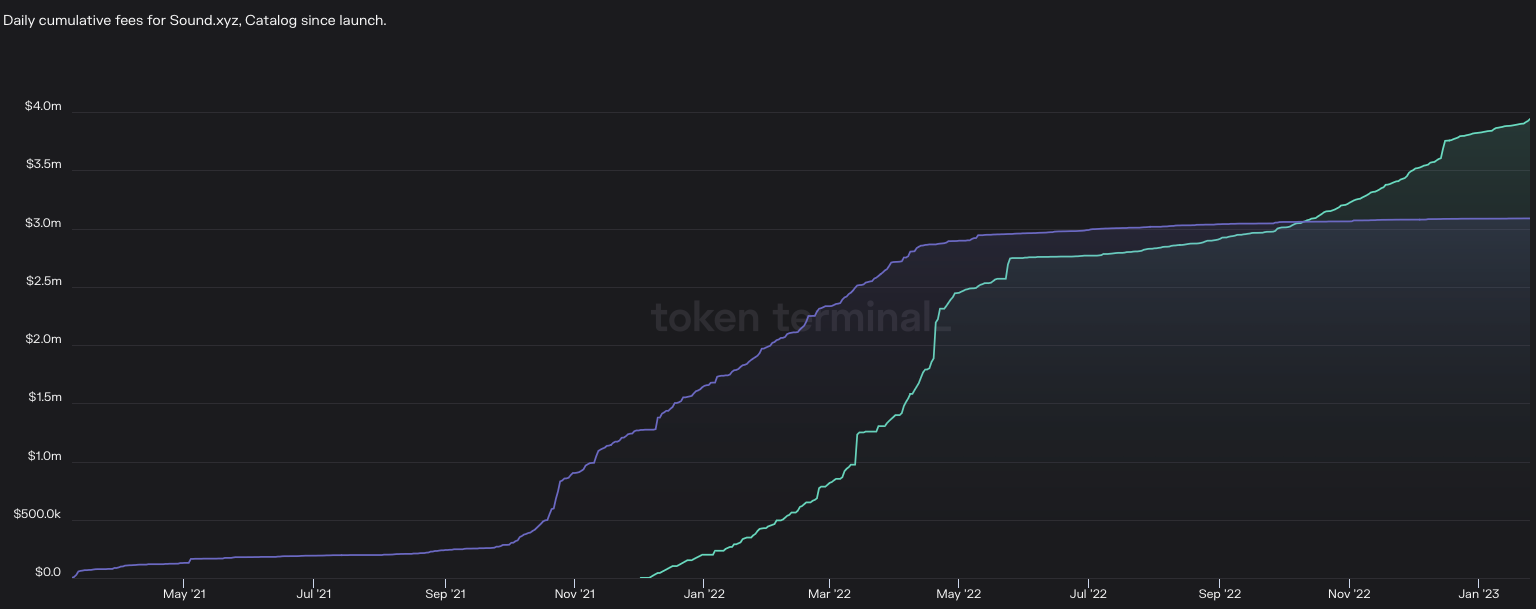

Catalog launched in March 2021 and focuses on single edition (1/1) drops (high exclusivity). It benefited from being early, but has since then lost ground to Sound. Monthly sales volume is in the range of $10-25k, down significantly from the peak of $600k (October 21).

Source: Tokenterminal Sound has a broader offering, combining the marketplace and minting with social elements, such as listening party and collector rankings. Since its inception in late 2021, Sound has generated ~$4.5m in total for artists. In contrast with Catalog’s drop in monthly sales, activity on Sound has kept growing steadily (both in terms of number of collectors and new drops).

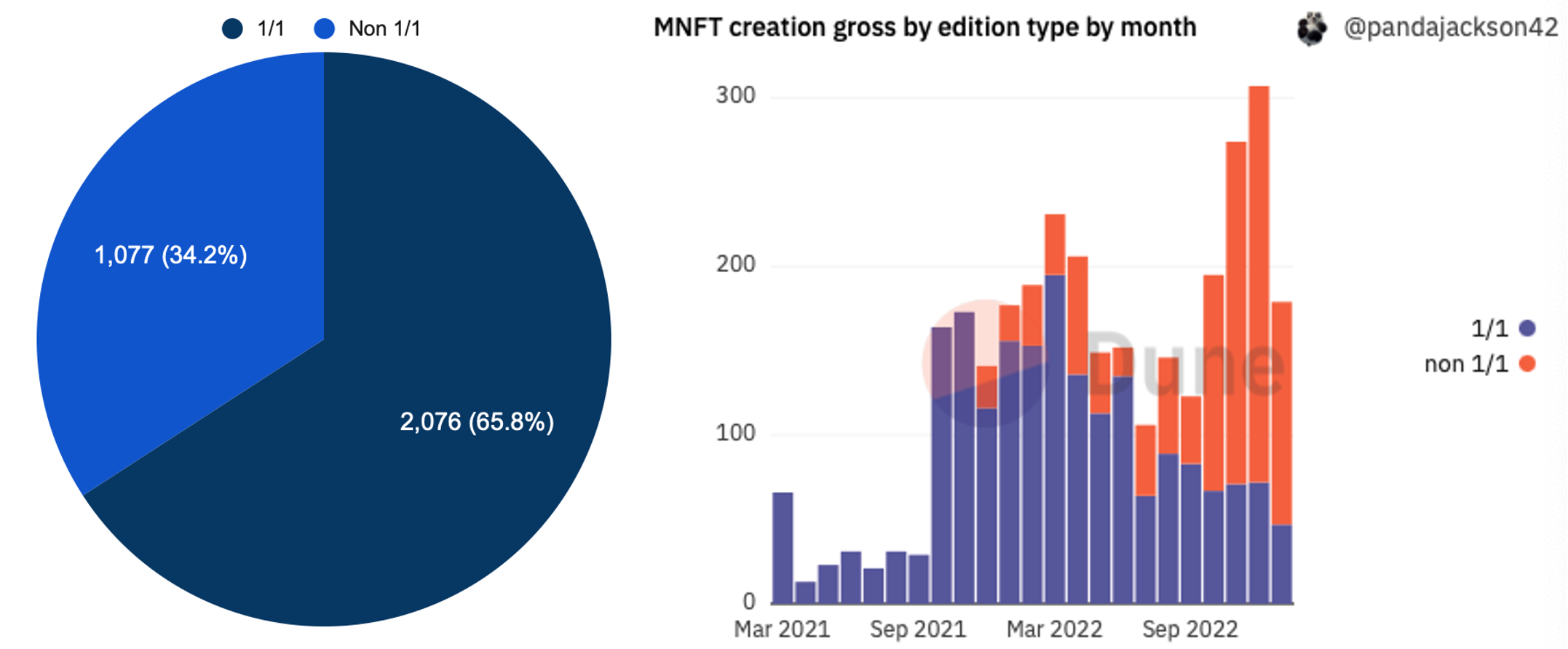

There are around 800 artists who have created ~3,200 different music NFT collections (on Sound, Catalog, Glass and Mintsongs). Approximately 2/3 of these are exclusive 1/1 editions, with the remaining being either limited- or open editions. There’s been a shift towards non 1/1 editions in the past 6 months as Sound has gained market share and I expect this trend to continue.

The average music NFT on these platforms sold for $156, which makes it fairly accessible for most people. We can see that secondary sales are on average 3.5x the primary, indicating that there is potential upside for the early collector. 1/1 editions are significantly more expensive due to their exclusivity. This is because the artist needs to make enough from just one sale, compared to selling a larger collection of 20-30 NFTs.

Source: Dune Despite the market downturn in 2022, there’s been a constant stream of new creators/artists entering to the space. This is an encouraging sign, as it indicates that artists are interested in exploring and want to be a part of the space.

This post has focused more on the benefit for emerging artists, but there are also established artists experimenting. Kings of Leon were one of the first major ones to launch an album in 2021, but others have followed (3LAU, Snoop Dogg, Weeknd…). I would expect to see more big artists dip their toes into the water over the coming months.

While disruption tends to come from the outskirts of an industry - the challengers rather than the incumbents - it doesn’t mean the incumbents are sitting still. For example, Warner Music Group (WMG) is partnering with LGND.IO to develop LGND Music. It’s a music NFT trading platform on Polygon, launching in January 2023. In an attempt to sidestep poor public perception around NFTs and crypto, they are calling the digital collectibles “Virtual Vinyls” rather than music NFTs. Conceptually, they are the same though.

5. Summary

A common misconception one might get from reading this post is that music NFTs are free money. Quite the opposite. Building a community takes a lot of time and effort. The fans that support you expect to get something in return. Releasing the NFT is only the start of the relationship, not the end.

While artist burnout is a real problem in the space, it’s always more difficult for the trailblazers than the followers. Much of this is trial and error, and there is a lot of experimentation. Most artists in the space still claim it’s worth it though. Without it, it’s likely they wouldn’t be able to keep doing what they love.